How to File Taxes

Understand the basics of tax filing as a freelancer

Understand the basics of tax filing as a freelancer

An official sales receipt is a proof of transaction issued by a business either to a customer or other businesses. Every time a sale is made, a receipt should be issued as an official transaction record to verify the amount paid by the buyer for the product or service. Issuing receipts and collecting every single one from every transaction that you make ensures that your income and expenses are correct, valid, and legal.

Only BIR-accredited printers can print Official Receipts that you can use for your business.

Bookkeeping is a set of financial activities that involve managing your financial records.

This includes the following activities:

Only BIR-stamped Book of Accounts or journals are considered official book of financial records.

Not issuing receipts or having an incomplete list of your sales, as well as your expenses may have the following consequences:

If these activities sound “business-y” for you, take note that self-employed individuals are also businesses. These activities are standard and part of a freelancer’s responsibility in managing your service business, and not just in filing your taxes.

Tax filing is the submission of tax forms to BIR in which you declare the amount of your income and the appropriate tax deduction according to your income bracket.

All Filipino income earners must register with BIR and legally declare what type of taxpayer they are based on their source/s of income.

For example, Employed taxpayers are registered as Purely Compensation Income earners, in which the employer handles their registration with BIR using form 1902.

On the other hand, self-employed taxpayers, such as freelancers and business owners, file the BIR form 1901 and register themselves as any of the following, whichever applies:

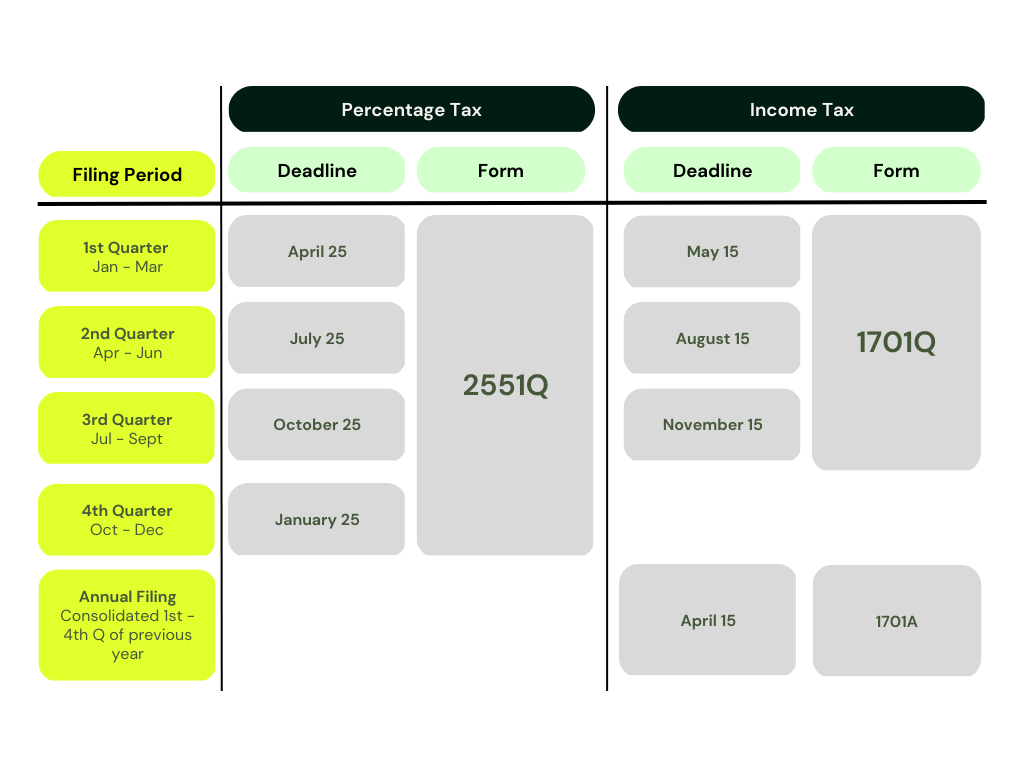

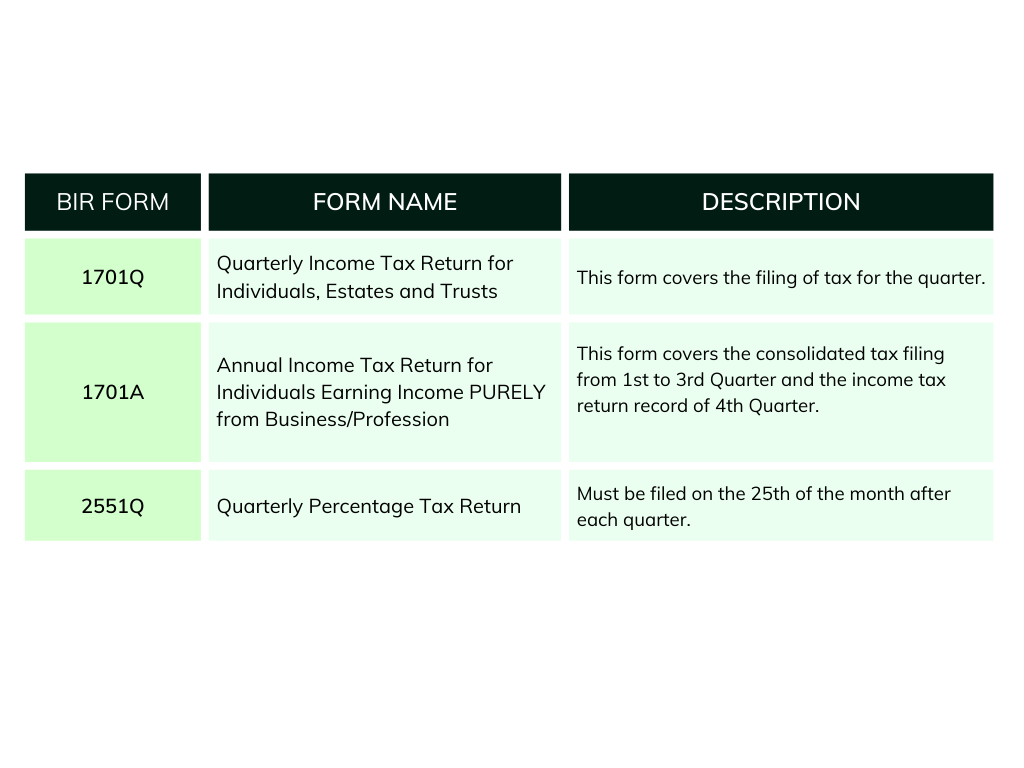

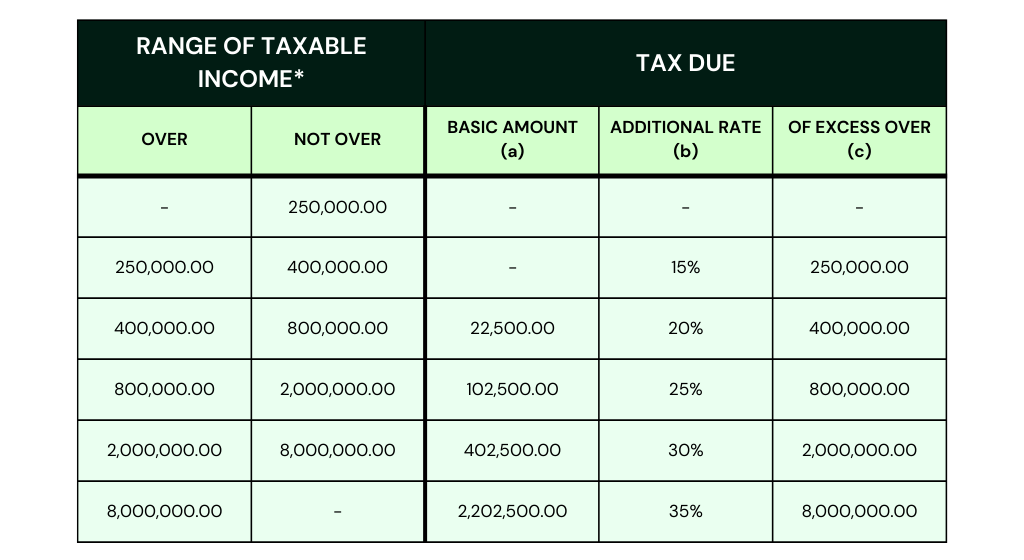

There are different types of taxes. Yes, you read that right. Taxes paid by one taxpayer may vary from another depending on their range of income. For self-employed professionals, the following types of taxes are usually paid:

The Graduated Income Tax Rate computes the allowed deductions from your tax by taking 40% of your income as expenses.

This tax method started with TRAIN Law and only applies to sole proprietors and professional, non-VAT earners. Now, small and micro self-employed professionals can pay a flat tax of eight percent on gross sales instead of the income and percentage tax quarterly.

Contractors who opt to use the Graduated Income Tax as a tax method, are required to pay the 3% quarterly percentage tax.

Important Note: Claiming the 8% Flat Income Tax Rate must be declared in the 1st Quarter filing or in the first quarter of the tax year when you start working with Remote Staff as a self-employed contractor. Otherwise, your tax type method shall default to Optional Standard Deduction.

Read more to learn how Remote Staff can assist you in doing your taxes!

Know about the tax responsibilities of a self-employed individual.

The information in this site for general guidance is not intended to replace or serve as a substitute for any audit, advisory, tax, legal, or other professional advice, consultation, or service. We strongly recommend that you consult an accountant before making any decision regarding your taxes. Remote Staff will not be responsible for your tax compliance as a result of the misuse or abuse of the content herein. You should not send any confidential information to Remote Staff until you have received agreement from the company to perform the services you request.